CORSIA compliance – the unequal choices that airlines face in the first phase

At a glance: We look at the challenges which an aircraft operator faces in complying with its obligations under the First Phase of CORSIA. To CEF or not to CEF? That is the question. In our view, this question revolves around the price of CEF and CEEUs and, in turn, supply and demand drivers for which presently there is a clear lack of information, data and price risk management tools.

Introduction

The International Civil Aviation Organization (ICAO) introduced the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) with the intention that aircraft operators monitor their emissions and offset excess emissions arising from covered aviation activity. The first phase of CORSIA (2024 to 2026) (the First Phase) has started. The First Phase remains voluntary but once an ICAO State commits to participate in the First Phase, compliance becomes compulsory for the aircraft operators1 for which that State is the responsible authority. 126 States have voluntarily committed to the First Phase of CORSIA. Notable non-participating States in the First Phase include China, Russia, India and Brazil. Broadly, only flights between participating States are caught by CORSIA. Participation in CORSIA becomes mandatory for all States in the second phase (2027 to 2035).

Aircraft operators with First Phase compliance obligations are actively looking at how they achieve this. CORSIA allows aircraft operators to meet their compliance obligations using either or both CORSIA eligible fuels (CEFs) and CORSIA Eligible Emissions Units (CEEUs). As things stand today, there are a number of supply, demand, pricing and regulatory challenges with respect to both CEFs and CEEUs that make the choices for aircraft operators particularly difficult. We consider the factors impacting those choices and looks towards market solutions that are in the pipeline to support the needs of the industry.

Please note that this paper recognises that more than one type of entity can be an ‘aircraft operator’ but is written on a neutral basis as to the type of entity (e.g. the ICAO Designator, AOC holder2 or aircraft owner3) that carries the compliance obligation. That said, we note that the risk management solutions adopted by the aircraft operator might differ depending on who they are.

Quick Summary of Key Concepts4

CORSIA Eligible Fuels

In essence CEFs are either (i) a CORSIA sustainable aviation fuel or (ii) a CORSIA lower carbon aviation fuel, which an aircraft operator may use to reduce their offsetting requirements. It should be noted that under Sustainability Criteria 1.1, in order for a fuel to be considered CEF, it needs to have net greenhouse gas emissions reductions of at least 10% compared to a baseline for an aviation fuel (the CEF Threshold).

CORSIA Eligible Emissions Units

CEEUs are those units described in the ICAO document entitled “CORSIA Eligible Emissions Units”, which meet the CORSIA Emissions Unit Eligibility Criteria contained in the ICAO document entitled “CORSIA Emissions Unit Eligibility Criteria”.5

Offsetting with CEEUs and CEF Reduction Claims

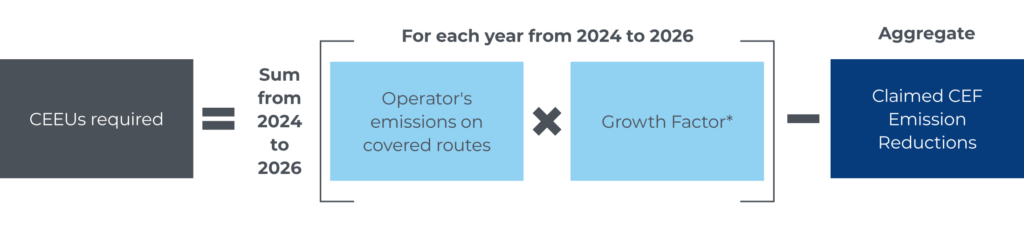

Broadly, an aircraft operator is required to cancel CEEUs at the end of the First Phase to offset its covered emissions. Where an aircraft operator also uses CEFs during the First Phase, CORSIA allows that aircraft operator to reduce its final total offsetting requirements at the end of the First Phase. Since CEFs are, to some extent, a substitute for CEEUs, their price should logically bear some relation to the price of CEEUs in terms of how an aircraft operator therefore manages its CORSIA compliance obligations.

(Simplified form of aircraft operator’s compliance requirements for the First Phase)6

* Growth factors are calculated by dividing the aggregated increase in total CO2 emissions above the baseline from all operators for the given year by the total CO2 emissions from international civil aviation in the given year. The baseline for 2030 will be 85% of 2019 emissions on the same state-pairs as those applicable in 2030.

Challenges to CORSIA compliance – as things stand today and what could change?

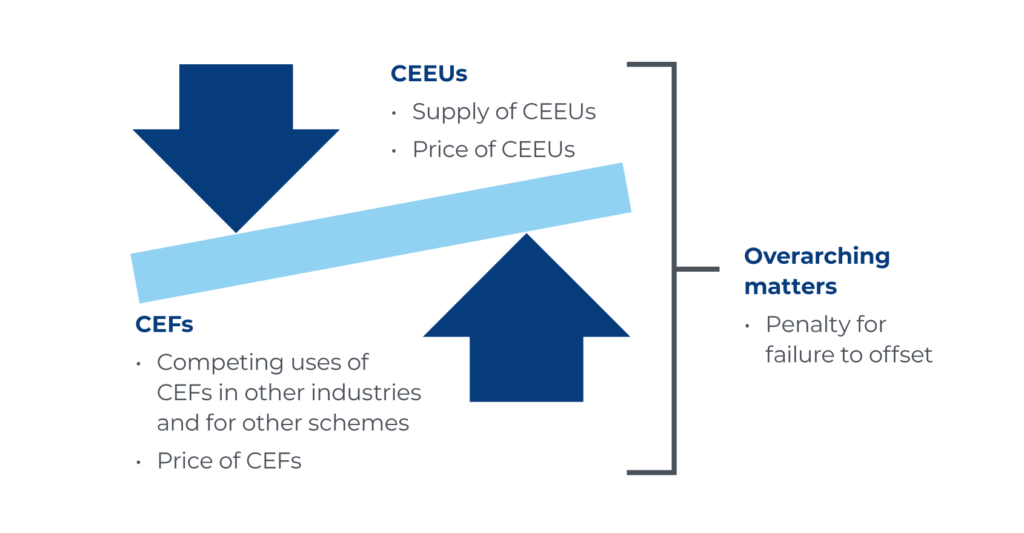

In weighing up how to comply with their CORSIA obligations, aircraft operators can choose between just using CEFs or just using CEEUs but, in reality, we expect aircraft operators to use a mix of both. The question of whether both solutions are progressed simultaneously or whether aircraft operators prioritise CEFs ahead of CEEUs, turns on a number of factors that reflect the state of play today in the market for CEFs and CEEUs. We discuss some of the factors, first in the context of CEFs and then in the context of CEEUs, below.

With time, these factors will no doubt shift and therefore their influence in the decision matrix of the aircraft operator will also shift.

In relation to CEFs, the aircraft operator’s decisions today and in the future may be influenced by the following:

| Decision points | Factors influencing an aircraft operator’s decision on CEFs | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Competing demand |

Situation today:

In the future:

|

||||||||||||

| Lack of supply |

Situation today:

In the future:

|

||||||||||||

|

Price of CEFs |

Situation today:

In the future:

|

||||||||||||

| Availability of deliverable CEF hedging contracts |

Situation today:

In the future:

|

In relation to CEEUs, the aircraft operator’s decisions today and in the future may be influenced by the following:

| Decision points | Factors influencing an aircraft operator’s decision on CEEUs |

|---|---|

| Competing demand |

Situation today:

In the future:

|

| Lack of supply |

Situation today:

In the future:

|

| Price of CEEUs |

Situation today:

In the future:

|

| Availability of deliverable CEEU hedging contracts |

Situation today:

In the future:

|

The commercial dynamics and conundrum for aircraft operators

With the aforementioned in mind, there are four potential paths for an aircraft operator to take in respect of its compliance requirements for the First Phase:

- Approach 1: Claim CEF emission reductions only

- Approach 2: Surrender CEEUs only

- Approach 3: Do a mix of 1. and 2., i.e. claim some CEF emission reductions and surrender CEEUs for the remaining emissions that the aircraft operator is liable for

- Approach 4: Do nothing – i.e. pay the penalty

The approach to be taken will likely be driven by commercial drivers.

Factors considered by an aircraft operator for First Phase offsetting obligations

Approach 4 is unlikely to be tenable once jurisdictions clarify the penalty regime for not offsetting emissions under CORSIA. To the extent that there are sufficiently robust penalties associated with this, e.g., a fine on top of the aircraft operator still having offset, as well as effective enforcement regimes (e.g., a fleet lien that allows the State to detain a defaulting aircraft operator’s fleet of aircrafts).

Approaches 1 to 3 will depend on the issues and drivers that we have already identified above, but ultimately it is invariably tied to the price of CEFs and CEEUs.

It has already been seen that some airlines have already opted to go with Approach 2 due to the current viability of CEFs. For instance, AirAsia CEO Tony Fernandes said in a shareholder letter that he intends to introduce a “sustainability levy” on airfares to purchase carbon offsets (i.e. CEEUs). He added that “while we support SAF, it must be economically viable and not burdensome to our passengers. The reality is that SAF is not yet a viable reality”, citing the costs and significant logistical challenges of SAF production.42

Nonetheless, as we discuss above, future developments could change the present position (e.g., those relating to future supply for CEF and CEEUs) and this can impact both present and future decision-making for an aircraft operator. For instance, managing supply constrains in the near term by locking in supply of CEF through offtake contracts.

Conclusion

The commercial dynamics at play here are both a challenge and an opportunity for aircraft operators. With the right preparation, CORSIA compliance costs can be managed in different stages (near term and future). Understanding how CORSIA fits in with other current, future and embryonic regulatory regimes enables aircraft operators to better understand how to maximise limited resources (CEFs and CEEUs) and manage price and supply risk.

Footnotes

- Defined as ‘aeroplane operator’ in Annex 16, Environmental Protection, Volume IV, Appendix 1 [CORSIA SARP]

- Each capitalised term as defined in Part I of CORSIA SARP.

- Defined as ‘aeroplane owner’ in CORSIA SARP.

- For the avoidance of doubt, we only discuss the position under CORSIA SARP, and not how it may have been implemented under national law.

- See CORSIA SARP, Part II, para 4.2.1

- Some notes: (i) the split between the individual component and sectoral component applies from 2033 to 2035 and thus does not apply for First Phase, and (ii) there are various factors to covered routes, e.g., state-pairs subject to offsetting requirements

- See https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/oil/120623-saf-production-to-triple-to-15-mil-mt-in-2024-but-progress-slow-iata

- Regulation (EU) 2023/1805 of the European Parliament and of the Council of 13 September 2023 on the use of renewable and low-carbon fuels in maritime transport, and amending Directive 2009/16/EC [FuelEU Maritime].

- IATA Net Zero 2050 – SAF Factsheet: see https://www.iata.org/en/iata-repository/pressroom/fact-sheets/fact-sheet—alternative-fuels [IATA Factsheet].

- For instance, Japan is planning a SAF mandate of 10% by 2030 (https://asia.nikkei.com/Business/Transportation/Japan-to-require-overseas-flights-use-10-sustainable-fuel) which has been estimated to mean demand for “approximately 1.7 million kiloliters of SAF annually” (https://www.resourcewise.com/environmental-blog/driving-change-in-aviation-japan-announces-10-saf-mandate).

- For instance, Singapore has a 1% SAF target from 2026, ramping up to 3-5% by 2030 (subject to global developments and the wider availability and adoption of SAF): https://www.caas.gov.sg/docs/default-source/docs—so/singapore-sustainable-air-hub-blueprint.pdf.

- See https://www.aapairlines.org/wp-content/uploads/2023/11/AAPA_PR_Issue14_AP67_Resolutions_10Nov23.pdf

- See https://news.delta.com/business-imperative-delta-outlines-roadmap-more-sustainable-travel.

- See e.g., Ben Elgin, Bloomberg (1 February 2024) “Sustainable Jet Fuel Supply Crunch Endangers Airlines’ Climate Targets”: “… the supply of SAF is likely to be 30% to 40% below the demand from airlines by the end of the decade, said Van Passel [head of procurement operations and development at Cathay Pacific]. “And we expect that gap to widen,” he added.” (https://www.bloomberg.com/news/articles/2024-01-31/cathay-pacific-sustainable-aviation-fuel-supply-crunch-endangers-climate-plan) [Bloomberg Article].

- Future availability of SAF via HEFA ‘likely overestimated’: MSCI (qcintel.com).

- See IATA Factsheet.

- https://www.reuters.com/sustainability/us-sustainable-aviation-fuel-production-target-faces-cost-margin-challenges-2023-11-01/

- Some of these thresholds will ramp up

- https://www.gov.uk/government/news/aviation-fuel-plan-supports-growth-of-british-aviation-sector

- See para 4 of The Renewable Transport Fuel Obligations Order 2007 (2007 No. 3072) (as amended).

- See Article 4(2A) of The Greenhouse Gas Emissions Trading Scheme Order 2020 (2020 No. 1265) (as amended) read with Art 54 of the Monitoring and Reporting Regulation 2018.

- See e.g., American Airlines 2023 Annual Report at page 19.

- See IATA Factsheet.

- See https://www.iata.org/en/pressroom/2023-releases/2023-12-06-02. The small percentage of SAF output as a proportion of overall renewable fuel is primarily due to the new capacity coming online in 2023 being allocated to other renewable fuels (linked to the demand discussion we had above).

- See https://www.offshore-technology.com/analyst-comment/saf-production-capacity-2030-predictions/

- which relies on inedible animal fats (tallow), used cooking oil and industrial grease as feedstock. There are limited quantities of these and thus a need to diversify SAF production by increasing production through pathways already certified, in particular the Alcohol-to-Jet (AtJ) and Fischer-Tropsch (FT) which use bio/agricultural wastes and residue, promote investments in, and the fast-tracking of certification for, new SAF production pathways currently in the developmental phase and identify more potential feedstocks to leverage all SAF technologies to provide diversification and regional options, including those with side-benefits such as environmental restoration: https://www.iata.org/en/pressroom/2023-releases/2023-12-06-02/

- When will Sustainable Aviation Fuel Get Cheaper? | AvBuyer; 1.5 to 6 times: https://www.easa.europa.eu/eco/eaer/topics/sustainable-aviation-fuels/current-landscape-future-saf-industry#production-capacity-and-demand-beyond-2030-to-2050

- See e.g., https://www.qcintel.com/carbon/article/airasia-eyes-offsets-from-new-fare-levy-over-burdensome-saf-24135.html

- See the Bloomberg Article where it was suggested that SAF is two or three times more expensive than conventional jet fuel.

- https://www.qcintel.com/biofuels/article/saf-hvo-saf-premium-steady-in-quiet-market-hvo-at-2-month-lows-25036.html.

- Immaturity of SAF market makes pricing stability difficult: Airlines (qcintel.com).

- See https://www.strategyand.pwc.com/de/en/industries/aerospace-defense/real-cost-of-green-aviation.html

- https://pubs.rsc.org/en/content/articlelanding/2024/se/d3se00978e

- https://www.easa.europa.eu/eco/eaer/topics/sustainable-aviation-fuels/current-landscape-future-saf-industry#production-capacity-and-demand-beyond-2030-to-2050

- See e.g., the CME listed FAME O Biodiesel FOB Rotterdam (Argus) (RED Compliant) Future and the ICE Futures US listed Biodiesel Outright – Los Angeles Sustainable Aviation Fuel (OPIS) Future.

- See United Airlines 2023 Annual Report at page 15.

- We discuss the reasons for this in a separate paper.

- For the pricing based on opportunity cost pricing for adjusted emission reduction credits (i.e. those that come with a corresponding adjustment), see: https://ppp.worldbank.org/public-private-partnership/library/corresponding-adjustment-and-pricing-mitigation-outcomes

- See e.g., Ghana:

- HFW acted for Abaxx in the structuring of this product.

- See https://lcds.gov.gy/guyana-announces-worlds-first-carbon-credits-for-use-in-un-airline-compliance-programme-corsia/. See also the March 2024 news announcement from ICAO: https://www.icao.int/environmental-protection/CORSIA/Pages/CORSIA-News.aspx“ICAO welcomes the announcement by Guyana for its authorization and issuance of CORSIA eligible emissions units for use by aeroplane operators in Phase 1 of CORSIA (2024-2026 compliance period).”

- AirAsia eyes offsets from new fare levy over ‘burdensome’ SAF (qcintel.com)

Download briefing

Download a PDF version of ‘CORSIA compliance – the unequal choices that airlines face in the first phase’