authors

Personal Property Securities Act 2009: Overview and implications for commodities trading

Briefing

18 August 2011

13 MIN READ

1 AUTHOR

The Personal Property Securities Act 2009 (Cth) (the PPSA) will come into force in October 2011. The PPSA is a major reform which will establish a single national regime to regulate ‘security interests’ in ‘personal property’.

The PPSA will have far-reaching consequences for those conducting business in Australia, including stakeholders involved in commodities trading. Businesses need to be aware that certain transactions which are not traditionally regarded as creating security may now give rise to a security interest that needs to be perfected under the PPSA. Title to, or ownership of, goods no longer offers sufficient protection. Failure to perfect a security interest will have severe consequences for the secured party if the party providing the security interest becomes insolvent.

What is the PPSA and why is it being introduced?

The PPSA replaces existing regimes for registering security interests in personal property, unifying over 70 separate Commonwealth, State, Territory and common law rules currently governing personal property securities. A number of existing registers will be abolished, and instead, the PPSA will create a single national register, the PPS Register, for the registration of security interests in personal property. Failure to register a security interest on the PPS Register (or otherwise perfect it) may mean that an interest in property is lost due to a subsequent transaction dealing with that property, even where a person still ‘owns’ the property (i.e. as a lessor or seller under retention of title).

What is a security interest?

A security interest under the PPSA is an interest in personal property provided for by a transaction that, in substance, secures payment or performance of an obligation, without regard to the form of the transaction or the identity of the person who has title in the property. For example, a seller will have a security interest in goods sold on a retention of title basis until the seller is paid by the buyer. Furthermore, a hirer of goods will have a security interest in the goods which are the subject of the hire arrangement.

There are also certain interests that are deemed to be security interests under the PPSA whether or not the transaction actually secures payment or performance of an obligation. Amongst others, a consignor who delivers goods to a consignee under a commercial consignment (where a consignor retains title to the goodsbut delivers them to a consignee to deal with those goods and both parties deal with those goods in the ordinary course of business) will be deemed to have a security interest in those goods.

What is a PMSI?

There is a certain category of security interest, known as a Purchase Money Security Interest, or PMSI, which affords holders additional priority rights. PMSIs include a security interest in collateral created by:

- A seller who has secured the obligation to pay the purchase price (i.e. a supplier who sells goods subject to retention of title).

- A person who provided the value to purchase the collateral (i.e. the security interests of a financier).

- The interest of a lessor or bailor under a PPS Lease (beyond the scope of this briefing).

- The interest of a consignor who delivers property under a commercial consignment.

Attachment, perfectionand insolvency

A secured party must ‘attach’ and ‘perfect’ their security interest in personal property. In most cases, attachment will occur when the parties enter into an agreement that creates a security interest (e.g. when a sales contract with a retention of title clause is executed between a buyer and a seller).

A secured party must then ‘perfect’ their security interest in order to preserve priority and ensure that the security interest is enforceable in the event of insolvency of the grantor (e.g. the buyer) or another enforcement scenario. If a security interest is not perfected, the “secured” party will be treated as unsecured creditor in the event of the grantor’s (i.e. buyer’s) insolvency.

There are four main methods of perfecting a security interest, including:

- Registration on the PPS Register.

- Taking possession of the collateral (other than by way of seizure).

- Having control of the collateral (control is limited to certain categories of financial assets).

- The temporary perfection rules under the PPSA.

In most cases, a secured party will perfect their security interest by registering it on the PPS Register.

The clear message is that in order to protect a security interest it is crucial that steps are taken wherever possible and practical to perfect that interest.

PPS Register

The PPS Register will be an electronic register that is expected to be available 24/7 to receive lodgements and enable searches to be carried out, for a fee. A limited number of existing registers will be automatically migrated to the PPS Register. Secured parties will be required to register their security interests within strict timeframes.

In certain circumstances a single registration will be able to cover multiple transactions. This means that, where it is common for a seller (who supplies on a retention of title basis) to make repeated supplies of property to the same buyer the seller may only need to lodge a single financing statement in respect of that buyer.

Priority rules

The PPSA contains detailed provisions dealing with priorities of security interests where there are competing security interests in the same collateral.

Generally:

- Security interests perfected by control (limited to certain financial assets) have the highest priority.

- PMSIs then enjoy a ‘super’ priority over other perfected security interests if certain conditions are met and if they are properly registered on the PPS Register within the required timeframe.

- Perfected interests have priority over unperfected interests.

- Priority between perfected interests amongst themselves, and unperfected interests amongst themselves, is determined on a “first in time” basis.

- Priority between unperfected interests is determined in order of attachment.

There are other specific priority rules dealing with different kinds of personal property (including rules imposed by other legislation). The priority rules can be displaced by secured parties who may enter into subordination agreements between themselves.

Agricultural security interests and priority rules

The PPSA also sets out specific rules relating to agricultural interests. The holder of a perfected security interest in crops will be given ‘priority’ over other holders of security interests in the same crops where he has:

- Provided value.

- The value has been provided to enable the crops to be produced.

- Either a security agreement is entered into while the crops are growing or the crops are planted within six months of the security agreement being entered into.

The most obvious example of this is a bank loan given to a grower to enable the grower to produce their crops, while the crops are growing or within six months after the loan has been provided.

Buyer protection

The PPSA sets out a number of rules where a buyer can take personal property free of any security interest.

One of the rules provides that where there is an unperfected security interest. A buyer who provides new value can acquire the collateral free of the security interest. For example, if a grower of a consignment of grain sells the grain to a trader on credit terms or where there is an intention to retain title in the grain until payment, but the grower fails to register its security interest and a third party buyer pays the trader for the goods (but the trader does not pay the grower), then the buyer will acquire the collateral (i.e. the grain) free of the grower’s security interest.

Another of the rules provides that a buyer can take personal property free of any security interest if it was sold in the ordinary course of the seller’s business of selling goods of that kind. The general rule is subject to exceptions, one of which includes where the buyer had actual knowledge the sale constitutes a breach of the security agreement that provides for the security interest.

Commingled goods

The PPSA also contains specific rules to deal with security interests in goods that become an unidentifiable part of a larger mass or product. For example, where grain is delivered by an individual grower to a bulk handler’s storage facilities and becomes commingled with other grain stored by the bulk handler. It is possible to perfect security interests in goods that subsequently become commingled. A security interest in goods that become commingled continues even where the identity of the original goods is lost. There are specific priority rules dealing with multiple security interests in a commingled product or mass. Note that that the value of the security interest in the mass is limited to the value of the original goods on the day on which they became part of the product or mass.

Proceeds of goods

Secured parties can specify in their security agreement that their security interest extends to the proceeds of the collateral. There are a number of rules setting out when proceeds are identifiable or traceable and when a secured party can seek to enforce their security interest in proceeds of the collateral, including in relation to proceeds of crops.

Note again that the amount secured by the collateral (and its proceeds) will be limited to the market value of the collateral immediately before the collateral gave rise to the proceeds.

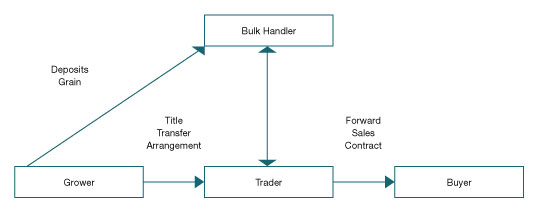

Worked examples of Australian grain trading transactions

Consider the above diagram (assume all transactions take place in Australia) and the following worked examples:

Grower’s perspective

The Grower’s grain has been delivered to, and is in possession of, the Bulk Handler on a consignment basis and the grain is commingled with grain stored by the Bulk Handler. The Grower enters into a title transfer arrangement with the Trader to be facilitated by the Bulk Handler.

The Grower will need to put appropriate arrangements in place to protect its security interest in the grain and consider, for example:

- Protecting itself in the event that the Bulk Handler were to become insolvent.

- Protecting itself in circumstances where possession of the consignment is transferred to the Trader prior to payment being received in the event that the Trader fails to pay or becomes insolvent.

Trader’s perspective

The Trader has purchased and paid for the Grower’s grain but is yet to take possession of or on-sell the grain. The Trader will need to put appropriate arrangements in place to protect its security interest in the grain and consider, for example:

- Protecting itself against the insolvency of the Buyer where the Trader sells and transfers the grain without immediate payment.

- Perfecting its security interest in the grain so that interest claim by the Bulk Handler is subordinated to the Trader’s security interest.

Buyer’s perspective

The Trader has not paid for the Grower’s grain under the title transfer arrangement. The Trader has on-sold that grain (as a portion of the Bulk Hander’s commingled storage of grain) to the Buyer by entering into a forward sales arrangement without taking physical delivery of the grain.

The grain remains in the Bulk Handler’s storage facilities until the Buyer takes possession of the grain from the Bulk Handler and pays the Trader in full. The Buyer will need to put appropriate arrangements in place to protect its security interest in the grain and consider, for example:

- Whether the Buyer may be faced with competing claims of the Grower or the Bulk Handler (i.e. for unpaid storage fees).

- Whether the Buyer can structure its arrangements to take advantage of any of the legislative protections under the PPSA in order to take the grains free from any other security interest.

(Note: Where the Buyer is a foreign entity, special foreign jurisdiction rules apply in respect of security interests regulated by the PPSA.)

Recommendations

We strongly recommend that businesses should:

For more information, please contact Aaron Jordan, Partner, on +61 (0)3 8601 4535 or aaron.jordan@hfw.com, or Chris Lockwood, Partner, on +61 (0)3 8601 4508 or chris.lockwood@hfw.com, or Hazel Brasington, Partner, on +61 (0)3 8601 4533 or hazel.brasington@hfw.com, or Stephen Thompson, Partner on +61 (0)2 9320 4646 or stephen.thompson@hfw.com, or Alexandra Birdseye, Associate, on +61 (0)3 8601 4549 or alexandra.birdseye@hfw.com, or your usual contact at HFW.

Download Briefing

Download a PDF version of ‘Personal Property Securities Act 2009: Overview and implications for commodities trading’

Related Insights

Briefing

Arbitration Act 1996: First Appeal To Succeed on All of Sections 67, 68 & 69

Briefing

Compliance with the Revised Port Marine Safety Code – Navigating the New Requirements

Briefing

EU ETS2 – Testing the Boundaries of Cap and Trade Systems

Briefing

SFO Launches Refreshed Corporate Guidance on Self-Reporting and Co-Operation

LATEST INSIGHTS

Briefing

Arbitration Act 1996: First Appeal To Succeed on All of Sections 67, 68 & 69

In what is, as far as we are aware, the first and only reported case of its kind, the Court has today allowed an appeal against an arbitration…

Read more

Bulletin

Comprehensively Yachts, May 2025 bulletin

Welcome to the Comprehensively Yachts semi-annual bulletin, featuring an array of insights and discussions on key topics within the yachting…

Read more

Briefing

Yachting in the Kingdom of Saudi Arabia

The dramatic coastline of the Kingdom of Saudi Arabia and in particular the Red Sea, with its crystal-clear waters and vibrant marine life is…

Read more