authors

In 2011, the European Union (EU) adopted Directive 2011/16/EU on the mandatory automatic exchange of information in the field of taxation in relation to reportable cross-border arrangements. Amendments have been made by Directive 2018/822 (EU DAC6) which introduces additional reporting requirements intended to assist the EU Member States (Member State(s)) to identify potentially aggressive tax arrangements. From a commercial perspective, EU DAC6 does not prohibit any kind of transaction but, rather, imposes an added level of transparency.

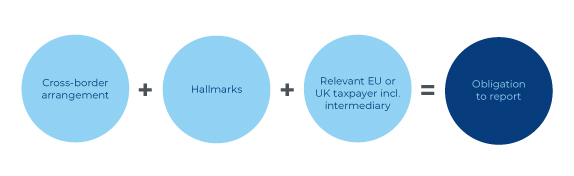

EU DAC6 requires disclosure to the relevant tax authority of all arrangements with:

In principal, the reporting obligation lies with the EU intermediary that designs, promotes, or implements the arrangement (e.g. tax advisors, accountants, lawyers etc.), but shifts to the taxpayer (i.e. the client) in certain cases (see Figure 1).

Mandatory disclosure will have far-reaching consequences both for us, as legal advisers, and for you, as our client. We, as the service providers in your transactions, will have to disclose any reportable arrangements to the relevant tax authority within 30 days from the date after our instruction on the transaction. In this Briefing, we go through the key features of EU DAC6 and provide guidance as to when reporting obligations arise (both for us as your lawyers, or for you directly).

The UK will adopt a UK version of EU DAC6 in early 2020 currently known as “The International Tax Enforcement (Disclosable Arrangements) Regulations 2020” (UK Regulations) regardless of whether or not it leaves the EU. The penalties for non-compliance could be quite onerous. Under the draft UK Regulations, these affect both the intermediary, if there is one, and the taxpayer and include:

N.B. Each of the EU Member States may adopt different penalties.

Please note that this area of law is still undergoing change and there may be slight variations between each of the Member States.

Figure 1: Reporting Obligations

For the purposes of EU DAC6, an arrangement is a cross-border one:

N.B. Even if a transaction is not a cross-border one initially, if there are changes to the structure, it may then become EU DAC6 reportable.

Any person that designs, markets, organises or makes available for implementation or manages the implementation of a reportable cross-border arrangement is an intermediary. An intermediary is, also, any person that knows or could be reasonably expected to know that they have provided such a function.

An intermediary can be an individual or a company, e.g. lawyers, accountants, consultants, banks, etc. Intermediaries must report information regarding the arrangement to the relevant tax authority in their Member State.

However, in the following situations, the reporting obligation shifts to the relevant taxpayer, i.e. the client as the person to whom the arrangement is made available:

A cross-border arrangement will be reportable if it falls within any of the Hallmarks. If an arrangement falls within categories A, B and certain subcategories under category C, it will only be reportable if it is also satisfies the Main Benefit Test. The Main Benefit Test is met if an expected tax advantage is the main benefit or one of the main benefits of an arrangement.

There are five Hallmark categories:

| Category A – Generic hallmarks linked to the Main Benefit Test |

|

| Category B – Specific hallmarks linked to the Main Benefit Test |

|

| Category C – Specific hallmarks related to cross-border transactions |

|

| Category D – Specific hallmarks concerning the automatic exchange of information and beneficial ownership |

|

| Category E – Specific hallmarks concerning transfer pricing |

|

Footnotes

|

Under the EU framework, intermediaries and taxpayers will have to report the following information regarding the reportable cross-border arrangement:

EU DAC6 will be effective as of 1 July 2020. However, taxpayers and intermediaries need to review cross-border arrangements from 25 June 2018, as they will have to report these by 31 August 2020. The first exchange of information between EU Member States will happen on 31 October 2020.

Please note that, from 1 July 2020 onwards, we as the lawyers, and therefore as the service providers in your transactions, have to disclose any reportable arrangements to the relevant tax authority within 30 days from the date after our instruction on the transaction. (Please see Figure 2: Timeline)

Figure 2: Timeline

EU DAC6 introduces new reporting requirements for transactions with a cross-border element. In the commercial world, this does not prevent businesses from carrying on their activities or entering into contractual relationships, which are, also, beneficial for tax purposes. Rather, the EU is setting up an automatic exchange of information platform between its Member States.

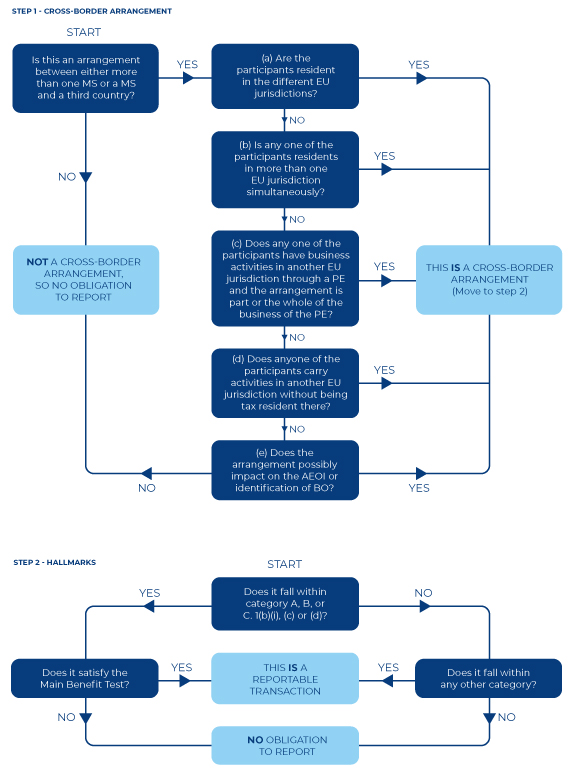

The new rules require a historical review of arrangements entered into from 25 June 2018 onwards. As of 1 July 2020, service providers, such as lawyers, will have to disclose any reportable arrangements to the relevant tax authority within 30 days from the date after their instruction on the transaction.The flowchart (see Figure 3) at the end of this document intends to help you determine whether your transactions are reportable by answering some simple questions.

Figure 3: Flowchart

As noted above, this area of law is very complex. HFW is happy to assist you with the analysis of your transactions; please contact our Risk & Compliance team or your usual HFW contact.

For further information, please contact the authors of this briefing:

Nick Hutton

Partner, London

T +44 (0)20 7264 8254

E nick.hutton@hfw.com

Sakina Chenot

Head of Legal Risk, London

T +44 (0)20 7264 8169

E sakina.chenot@hfw.com

Download a PDF version of ‘Cross border transactions into the EU or UK: will you be caught by the new DAC6 reporting requirements?’